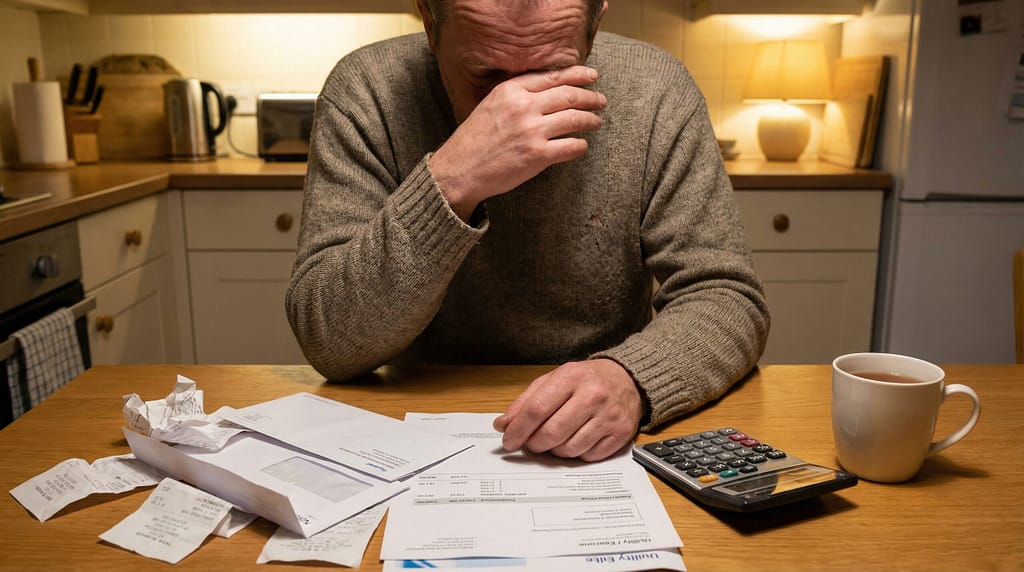

For two years I lived paycheck to paycheck.

Not because I had a low income. I earned a reasonable salary. Enough that I should have been fine.

But the money came in and then it just — went. I was never really sure where. I’d check my account on day 25 of the month and feel that specific kind of dread that anyone who’s lived this knows intimately. A tight chest. A quick calculation. Will it stretch?

I tried budgeting. Multiple times. Every attempt ended the same way — I’d track my spending for two weeks, realize how bad it was, feel overwhelmed, and quietly give up.

Then a friend asked me one question that completely reframed everything. She said: ‘Are you budgeting to track what happened or to decide what’s going to happen?’

I was doing the first one. That’s why it wasn’t working.

Why Paycheck to Paycheck Happens — The Real Reasons

Here’s something important: living paycheck to paycheck is not always an income problem. Studies consistently show that people at all income levels — including people earning $100,000 a year — can be trapped in this cycle.

The real causes I’ve seen again and again:

- No written budget: Money flows out without anyone consciously deciding where it goes

- Lifestyle inflation: Every time income went up, spending went up to match it automatically

- No emergency fund: Every unexpected expense becomes a crisis that wipes out any progress

- Subscription creep: Small recurring charges quietly accumulating to hundreds a month

- Saving what’s left: Which is usually nothing, because spending expands to fill available income

None of those are character flaws. They’re habits and systems — and habits and systems can be changed.

Step 1: The Uncomfortable Audit

I know. You probably already know roughly how bad it is. That’s exactly why looking at it properly feels so unpleasant.

Do it anyway. Pull up your last two months of bank statements. Go through every transaction. Don’t judge. Just categorize.

What you’re looking for:

- Every subscription you pay — list them all. Every single one.

- Your total dining and takeaway spend — add it up properly, including the ones that seem small

- Any purchase you made that you can’t remember or don’t care about now

- Any service you’re paying for that you’re not actively using

When I did this audit I found £340 per month in spending I was completely unconscious of. A meditation app I’d forgotten about. A cloud storage service running alongside one I actually used. Takeaway orders I’d completely forgotten making.

Step 2: Build the Bare-Bones Budget First

When you’re paycheck to paycheck you don’t have the luxury of a gentle budget. You need a survival budget — stripped back to what actually matters — at least temporarily.

Keep These

- Housing — rent or mortgage

- Essential utilities — electricity, gas, water, basic internet

- Basic groceries — no premium brands, no meal kits, no delivery fees

- Essential transport — minimum fuel or transit pass to get to work

- Minimum debt payments — to protect your credit and avoid fees

Cut These For Now

- All streaming services except one

- Dining out and all takeaways — completely, for 60 days

- Gym membership if you’re not going regularly

- All subscription boxes

- Non-essential shopping of any kind

This isn’t permanent. It’s a 60 to 90 day reset to create breathing room. Once you have breathing room you can add things back intentionally.

Step 3: The $500 Emergency Fund First

This is the most important single step to breaking the paycheck to paycheck cycle and it’s the one most people skip because it seems counterintuitive.

Before extra debt payments. Before investments. Before anything — build $500 in an emergency fund.

Here’s why. The paycheck to paycheck trap is self-perpetuating because every unexpected expense sends you into debt or overdraft, which costs you fees and interest, which makes the next month harder. The $500 buffer breaks this loop.

Car repair comes in at $400? Emergency fund handles it. No debt. No overdraft fees. No crisis. The cycle breaks.

Step 4: Budget by Paycheck, Not by Month

Monthly budgets work well for people with stable, predictable expenses. When you’re paycheck to paycheck the margins are too tight for monthly thinking.

Instead: when your paycheck arrives, allocate it immediately. Right now. Before you spend anything.

- Rent or mortgage: transfer this immediately or earmark it

- Fixed bills due before next paycheck: pay them or set aside the exact amount

- Groceries for the period: allocate a specific amount — take it out in cash if that helps

- Transport: fuel or transit money for the period

- Everything remaining: divide by days until next paycheck — that’s your daily spending limit

This method eliminates the classic paycheck to paycheck mistake — spending freely in the first week and having nothing left by week three.

Step 5: Find Even $100 Extra Per Month

On a tight budget, an extra $100 per month feels transformative. Here’s the fastest ways to find it:

- Sell 5 items from your home — Facebook Marketplace — this week

- One weekend evening of food delivery: DoorDash or Uber Eats — $80 to $120 for an evening

- Negotiate one bill: call your phone or internet company and ask for a better rate — works more often than you’d think

- Return one unused recent purchase — instant money back

- Offer one service to a neighbor — lawn, cleaning, babysitting — $50 to $100 for a few hours

The Thing Nobody Tells You About Breaking the Cycle

It doesn’t happen in one month. It usually doesn’t happen in two.

Month one you build the bare-bones budget and find it uncomfortable. Month two feels a little less uncomfortable. Month three something shifts.

My shift happened in month three when I checked my account on day 25 and instead of that tight-chest dread — I felt nothing. Because I knew exactly what was there. I’d planned for it at the start of the month.

That absence of anxiety was the moment I knew the cycle was breaking.

Quick Answers

How do you save money when you’re paycheck to paycheck?

Start with $25. Genuinely. Automate a $25 transfer on payday to a separate account you don’t touch. Most people paycheck to paycheck think saving is impossible — but $25 on payday before anything else disappears usually turns out to be possible. Then increase it by $25 each month.

Is living paycheck to paycheck normal?

Nearly 60% of Americans report living paycheck to paycheck — so statistically yes, it’s common. But common doesn’t mean it has to be permanent. Every person I know who has broken the cycle did it with some version of the steps above, and most did it within 6 months.

You might also like: How to Make a Budget for Beginners | Zero-Based Budgeting for Beginners | How to Save $500 in 30 Days | How to Get Out of Debt on Low Income