A friend of mine — sensible person, not financially reckless at all — had £35,000 in savings sitting in a regular easy-access savings account.

She thought she was doing everything right. She’d found a decent rate. She was saving consistently.

What she hadn’t considered was the tax. As a higher-rate taxpayer with £35,000 earning 4.8% interest, she was generating £1,680 per year in savings interest. Her Personal Savings Allowance as a 40% taxpayer is just £500.

She was paying Income Tax on £1,180 of that interest every year. At 40% that’s £472 in unnecessary tax. Every year. Just because her money was in the wrong type of account.

Moving it to a Cash ISA — which takes about 15 minutes — would save her £472 annually with zero other changes.

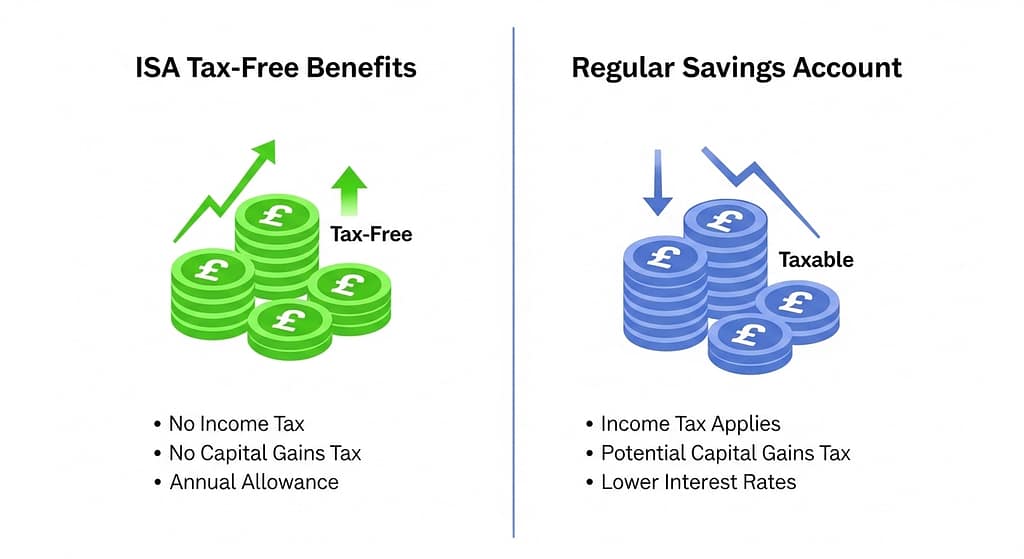

The Core Difference — and It’s Important

A Cash ISA is not a different kind of savings product. It’s a tax-free wrapper around a savings account.

Inside a Cash ISA: all interest is completely tax-free. Forever. No matter how much accumulates.

Inside a regular savings account: interest above your Personal Savings Allowance is taxed at your income tax rate.

The Personal Savings Allowance — Most People Underestimate This

- Basic rate taxpayer (20%): £1,000 per year tax-free savings interest

- Higher rate taxpayer (40%): just £500 per year tax-free

- Additional rate taxpayer (45%): zero allowance

With savings rates now at 4.5% to 5%, you only need £20,000 to £22,000 saved to breach the basic rate allowance at 5% interest. More than that and you’re paying tax on savings interest that could easily be sheltered in an ISA.

When a Cash ISA is Clearly Better

- You’re a higher rate taxpayer — your allowance is tiny, an ISA is almost always better

- You have more than £20,000 in savings — you’ll likely exceed the basic allowance

- You’re a long-term saver — the tax-free compounding becomes very significant over a decade

- You expect your income to increase — protecting savings in an ISA now keeps the tax-free status as your rate rises

When a Regular Savings Account Might Win

- The rate is significantly higher — 0.5% or more — and you won’t exceed your PSA

- You want to save more than £20,000 this tax year — ISA limit is £20,000 annually

- You want a regular savings account requiring monthly deposits for higher rates

Best Cash ISA Rates Right Now

As of January 2025 — always verify directly with providers as rates change:

- Plum Instant Access Cash ISA: around 5.17% AER — one of the highest flexible ISA rates

- Trading 212 Cash ISA: around 5.10% AER — excellent, flexible instant access

- Chip Cash ISA: around 4.84% AER — easy to open, instant access

- Paragon Bank Cash ISA: around 4.65% AER — traditional provider, FSCS protected

The Stocks and Shares ISA — Worth Mentioning

If you won’t need the money for 5 or more years, a Stocks and Shares ISA typically outperforms a Cash ISA significantly over time. All growth and dividends are completely tax-free. Providers like Vanguard, Fidelity, and Trading 212 all offer these with low fees.

Can I have both an ISA and a regular savings account?

Yes, absolutely. Most sensible UK savers do exactly this. Use your ISA allowance (£20,000 per year) for the bulk of your savings, and use a regular account for any amounts above that limit or for accounts with significantly better rates.

What happens to my ISA when the tax year ends?

Your ISA allowance resets every 6 April. Money already in your ISA stays there and keeps earning tax-free. You simply get a fresh £20,000 allowance for the new tax year. Unused allowance cannot be carried forward.

You might also like: Best Savings Accounts UK 2025 | How to Improve Credit Score UK Fast | Side Hustles UK 2025 | Best Cashback Apps UK 2025